Africa's Pensions Pitfall

Africa’s demographic dividend could have a sting in its tail if countries don’t manage to deliver higher savings rates and stronger economic growth

Africans are young. 28 of the 30 youngest countries in the world are found in sub-Saharan Africa. Much has been written about this so called “Demographic Dividend” as an engine of growth for the continent. Ensuring this blessing does not become a curse for pensions has received less attention.

Having a young population initially makes funding a pension scheme easy because you have plenty of working age people to support retirees; in technical terms you have a low old-age dependency ratio. However, if fertility rates fall then as this demographic bulge makes its way through the age bands and eventually arrives at retirement, you suddenly have a lot of old people who need to be supported by not so many workers; the old-age dependency ratio rises.

Though the average African is very young now, they won’t always be. In fact, fertility rates in sub-Saharan Africa have been falling for decades now from a peak of 6.8 births per woman in the late 1970s and early 1980s, to 4.7 in 2021. If this continues to fall, as many think it will (see China for example), then countries may well be facing a pensions crisis down the line. For example, the share of the population over 60 years old is expected to more than double in Kenya by 2050. The demographic dividend may have a sting in its tail.

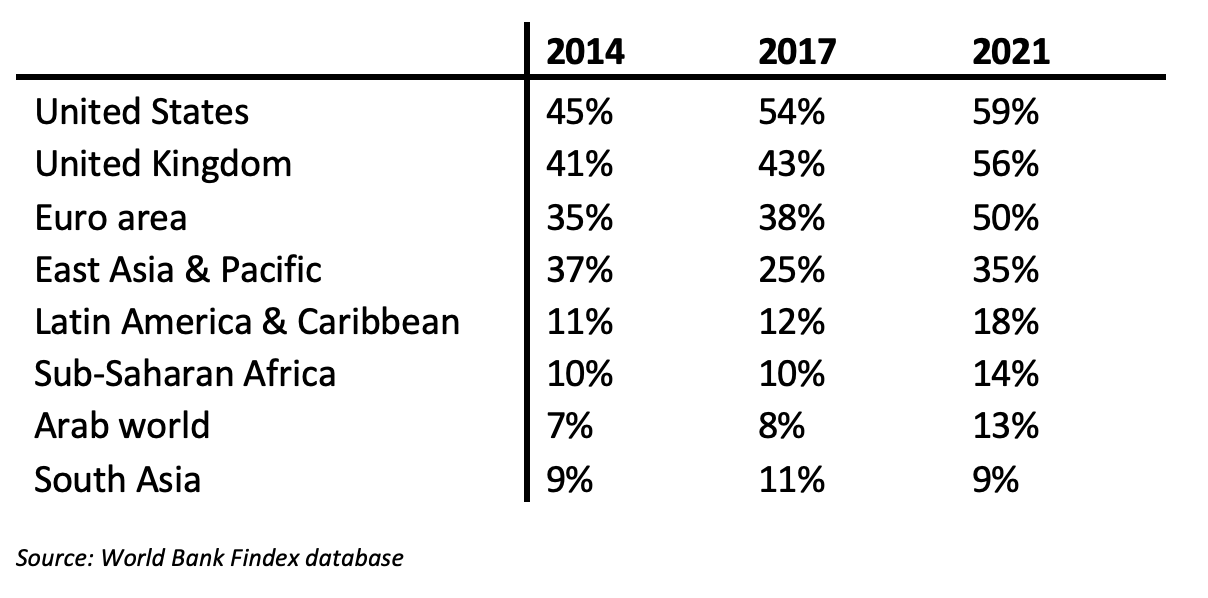

Very few Africans are saving for old age.

The antidote is strong national pensions schemes. At its simplest, this means a good share of adults saving for retirement. Unfortunately, the data on this are not particularly encouraging. According to the World Bank, just 14% of adults in sub-Saharan Africa report saving for retirement (although encouragingly this is up from 10% in 2017).

Table 1: share of adults (15+) saving for old age

Worryingly, the bar for being counted as “saving for old age” is low. World Bank researchers just asked people if they had saved or set aside any money in the past year for old age. This means 86% of adults in sub-Saharan Africa have saved literally nothing in the last year for old age. And evidence suggests that those who do save, don’t save much. For example, the average pension lump sum pay out in Uganda is reported to be UGX 13 million, or about $3,500 (worth less than five years of average annual income).

A tale of poverty and informality

None of this is particularly surprising. There are two main drivers of these worrying stats. One is poverty. People living in poverty are forced to focus on feeding themselves today and tomorrow, not decades down the line.

The other is informality. A far higher share of the workforce in sub-Saharan Africa is in the informal sector, making it difficult for formal pension schemes to operate. Some might say we don’t need to worry because Africans in the informal sector have developed equally informal mechanisms for dealing with retirement. They have lots of children or they buy land, the argument goes, so they don’t need proper pensions.

But if that’s true, why are Africans so worried? More than half of respondents in sub-Saharan Africa told those same World Bank researchers that they were “very worried” about not having enough money for old age, compared to just 1 in 5 of those asked in the US and Europe.

Table 2: share of adults (15%) worried about not having enough money for old age, 2021

Progress in formal pension schemes won’t be enough.

What can be done? Pensions policy has a natural tendency to focus on the formal sector. And progress in this regard has indeed been encouraging. An article published in the Economist in 2021 highlights the introduction of a new mandatory scheme for formal employees which has helped increase the value of pension funds in Nigeria 9-fold to $15 billion. South Africa also enjoyed some success through pumping cash into its civil service pension scheme.

But the formal sector simply isn’t big enough in many sub-Saharan countries for this it to be a sufficient remedy. For example, despite its impressive growth, the value of pension fund assets in Nigeria is still only around 8% of GDP. The value of pension fund assets is typically between 5 and 15% of GDP in sub-Saharan African countries, albeit with a few notable exceptions. Yet most advanced countries have pension fund assets larger than their GDPs.

Micro-pensions to the rescue?

Policymakers will need to go beyond the low hanging fruit in the formal sector and massively boost savings rates in the informal sector. One potential solution is micro-pensions. These typically are flexible schemes where informal workers can pay in small contributions when they are able to. The challenge of these, given the low amounts saved, has always been to keep administration costs low enough for it to be worthwhile. But the arrival of new technologies, especially mobile money, is helping.

For example, M-Pesa is crucial to the Mbao micro pension scheme in Kenya. This scheme targets “jua kali” (“blazing hot sun” in Swahili) workers (organised in the Jua Kali Association) in the informal sector, requiring them to make very small but regular savings through their phones. These savings are then pooled and invested.

In 2018, Rwanda launched Africa’s first completely digital, government-backed micro-pension scheme, known as EjoHeza. The scheme goes to great lengths to cater for the needs of informal workers. People can open a pensions account even with a simple feature phone and the scheme allows for flexibility in terms of size and frequency of contributions. Contributors can also access some of their funds for emergencies before retirement, a key concern for informal workers. Importantly, it leverages Rwanda’s investment in digital infrastructure, particularly its Central Administration IT Platform, which allows for seamless portability and low transaction costs (for more, see here). As a result, EjoHeza has enjoyed considerable success, attracting 1.4 million savers. Not bad for a country with a population below 14 million.

Governments have a role to play as well. There is much they can do to give these kinds of schemes a lift, including by offering incentives and subsidies. The Rwandan government, for example, matches contributions by poor and vulnerable people in the EjoHeza scheme. Given pensions are in many ways a public good that is undervalued by the population, the case for government support is strong. Effective regulation and consumer protection can also help by building confidence in these products.

Without economic growth, we face an uphill battle.

The novel schemes we see popping up across sub-Saharan Africa are important. They bring more people into the formal financial sector and they also help address the chronically low savings that hold back productive investment in these countries (high domestic savings rates were a big part of the development story for the East Asian Tigers). But it’s hard to escape the fact they are fighting an uphill battle. Many people in these countries just don’t have enough money to take care of their immediate needs and save for a distant future (the idea that some are “too poor to save” is well established). No matter how innovative they are, micro-pension schemes really struggle to escape this simple truth.

The Mbao scheme still has only 100,000 savers, despite being promoted to all the Jua Kali Association’s 12 million members. For many of Kenya’s informal workers, the daily contribution of $0.19 is enough to put them off. Another micro-pension scheme in Nigeria hoped to have reached 8 million informal workers in its first five years. It managed under 78,000, with the low incomes of target workers again blamed.

We come back to the need for economic growth, a familiar refrain for GPI’s regular readers. A growing economy gives the pension sector a massive boost – addressing both poverty and informality. As countries become richer their financial systems mature, the formal sector grows, and people have more money to set aside for a pension. No doubt we must continue to develop inventive ways to help informal workers save for old age. But let’s not forget, what they really need to save for tomorrow is higher incomes today.